The Foreign Investment Law sets aside the issue of VIE structures, but leaves a possibility for the VIE with a catch-all clause.

The VIE structure is commonly used to circumvent China’s foreign investment restrictions in some sensitive sectors. The legitimacy and stability of VIE structures have always been the focus of foreign investors. However, the PRC Foreign Investment Law promulgated in Mar. 2019 remains silent on whether the VIE structure should be included in the regulatory scope of foreign investment. This post will give a basic introduction to the VIE structure, and will briefly review the legislative evolution of this issue in the Foreign Investment Law and forecast the future regulatory attitude.

I. A Brief Introduction of the VIE Structure

1. The Application of VIE Structures in China

Variable interest entity (“VIE”) is a term first used by the United States Financial Accounting Standards Board (FASB) in Interpretation No.46. In China, VIE Structure is also referred to as “agreement-based control”, which means a listed foreign entity controls a Chinese company through a series of contractual arrangements, in order to circumvent China’s restriction and regulation on the initial entrance of foreign investment, foreign mergers and acquisitions, and overseas listing.

In China, this mode was firstly used in 2000. At that time, China’s Internet news company Sina listed in the United States, which made itself a foreign-invested company. In order to circumvent the Chinese government’s restrictions on foreign investment in the value-added telecommunications industry, Sina adopted the VIE structure.

In the following ten years, VIE structures provided a mature model for Chinese Internet companies (Tencent, Baidu, Youku, RENN, Jiayuan, Tudou, etc.) to successfully list in the United States, and also became a magic weapon of Chinese Internet companies for overseas capital operation.

Therefore, VIE plays an important role in the development of industries where foreign investment is restricted, such as the Internet industry. If the legality of the model is denied, these restrictions may cause the slowdown or even stagnation of many foreign investment-restricted industries. Consequently, the Chinese government and the regulatory authorities have always implicitly acknowledged the legitimacy of the VIE model.

2. Typical VIE Structures

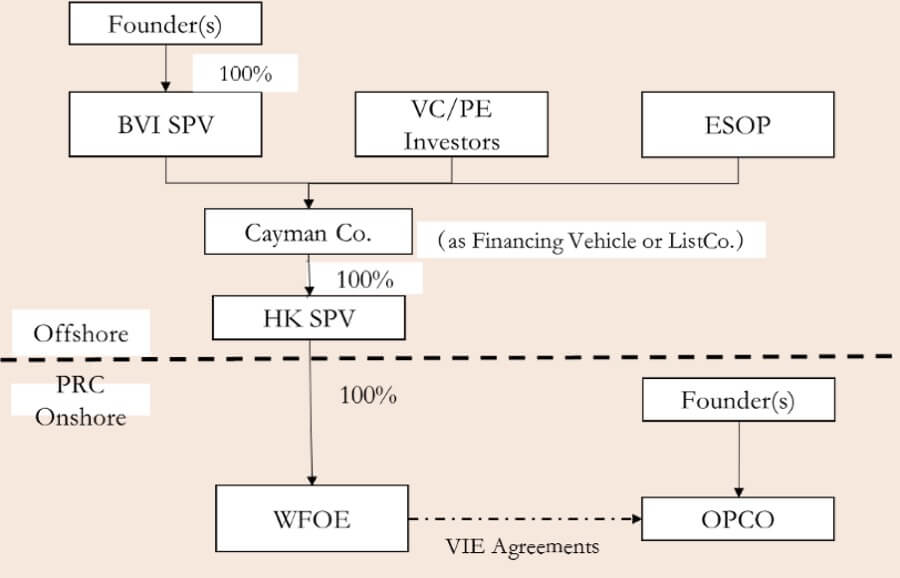

A typical VIE structure generally includes the following four main parts.

- A Chinese company works as the actual domestic operating company (“OPCO”), running the business in which foreign investment is forbidden or restricted, but has the need for overseas financing or listing.

- The founders of the company generally set up a company in the British Virgin Islands as the shareholder (BVI SPV), and a company (“Cayman Co.”) in the Cayman Islands for future listing (“ListCo.”). Before going public, the Cayman Co., as a financing platform (“Financing Vehicle”), can also introduce financial investors (“VC / PE Investors”) to raise funds for the company’s development. At the same time, the Cayman Co. will also set up an employee stock ownership plan (“ESOP”). The Cayman Co. will further establish a wholly-owned subsidiary in Hong Kong (“HK SPV”). Then the HK SPV will set up a wholly foreign-owned enterprise (“WFOE”) in China.

- The WFOE will sign a series of agreements (“VIE Agreements”) with the OPCO and its shareholders, including “Equity Pledge Agreement”, “Business Operation Agreement”, “Exclusive Service Agreement”, “Entrusted Voting Agreement”, and “Exclusive Option Agreement”, etc. Although there is no direct equity control between the WFOE and the OPCO, by concluding VIE Agreements, the WFOE can actually control the OPCO and obtain the profits from the OPCO’s operation.

- Through these agreements, Cayman Co. ultimately controls the OPCO and its shareholders, making it operate in accordance with the will of Cayman Co., and ensure that the operating profits of the OPCO will be transferred to overseas Cayman Co. after tax payment.

II. The Foreign Investment Law Sets Aside the Issue of VIE Structures

The Ministry of Commerce posted the PRC Foreign Investment Law (draft for comments) in Jan. 2015 (“2015 Draft for Comments”). In the 2015 Draft for Comments, VIE Structure was clearly recognized as a mode of foreign investment, thereby incorporated in the regulation of foreign investment. Article 15 stipulated that foreign investors controlled or held rights of a domestic company by means of contracts, trusts or other methods shall be deemed as foreign investment, and it was subject to the provisions about the initial entrance, security review, and information reporting in the Foreign Investment Law. Article 18 provided that “control” included methods such as agreements, trusts, or any other means which can exert a decisive influence on the business, finance, personnel, or technology.

However, the PRC Foreign Investment Law (Draft) posted on 23 Dec. 2018 (“2018 Draft”) did not mention the VIE Structure in 2015 Draft for Comments. Instead, a new catch-all clause about foreign investment methods was added: “Foreign investors invest in China by means of other methods stipulated by laws, administrative regulations or provisions of the State Council”. In other words, as the 2019 Foreign Investment Law followed the text of 2018 Draft, the legitimacy of VIE Structure and its regulation were put back on hold again.

III. An Expectation of Future Regulation

The Foreign Investment Law avoids to stipulate the legitimacy and the regulatory mode of the VIE Structure, but leaves a possibility for the VIE with a catch-all clause. However, we believe that the administrative authorities may only set regulatory pilots in specific sensitive sectors to prevent the circumstance of investment restrictions in these areas, such as in private education (which will be introduced in detail in Foreign Investment Law Series -07); but may remain tacit about the legitimacy of VIE Structure in most other areas.

Photo by Roman Voronin(https://unsplash.com/@imvoronin) on Unsplash

Contributors: Xiaodong Dai 戴晓东